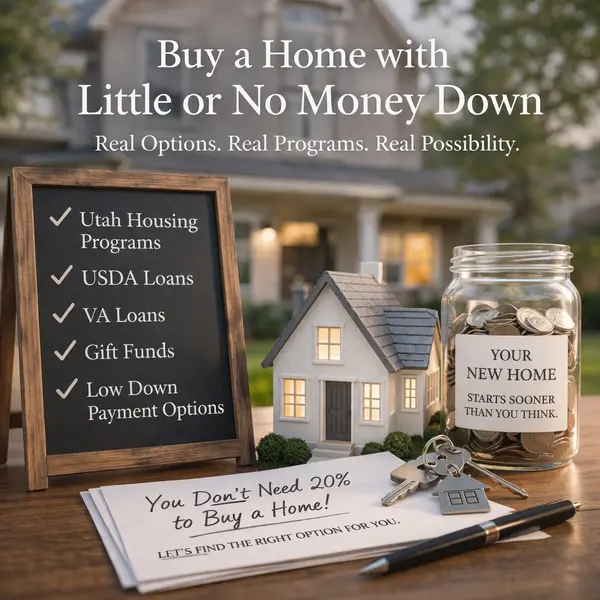

How To Get a Home Loan with Bad Credit

How to Get a Home Loan with Bad Credit (2026 Guide)

Real Options for Buying a Home-Even If Your Credit Isn’t Perfect

Many buyers believe you need perfect credit and a large down payment to qualify for a mortgage.

That’s simply not true.

In today’s market, there are several loan programs designed to help buyers with lower credit scores and limited savings become homeowners. While stronger credit gives you more options and better rates, “bad credit” doesn’t mean you’re out of the game.

Here’s what you need to know.

Loan Options for Buyers with Lower Credit

1. FHA Loans (Most Common Option)

FHA loans, backed by the Federal Housing Administration, are one of the most accessible paths to homeownership.

Typical guidelines (2026):

- Minimum credit score: 580 (for 3.5% down)

- Credit scores 500–579 may qualify with 10% down

- Down payment: as low as 3.5%

- Debt-to-income (DTI): typically up to 43%, but some approvals go higher with strong compensating factors

💡 Why buyers choose FHA:

Flexible credit requirements and lower down payment options.

2. VA Loans (For Eligible Veterans & Service Members)

If you’re a veteran, active-duty service member, or eligible military family member, VA loans are one of the best options available.

Key benefits:

- No down payment required (in most cases)

- No private mortgage insurance (PMI)

- More flexible credit guidelines (no official minimum set by VA, but lenders often look for ~580–620+)

📌 Eligibility is based on service requirements (which vary slightly), and a Certificate of Eligibility (COE) is required.

💡 Why buyers choose VA:

Lower upfront costs and flexible qualification standards.

3. Conventional Loans (Possible with Lower Credit)

Conventional loans typically require higher credit, but options are expanding.

- Some programs allow credit scores as low as 620

- First-time buyer programs may offer 3% down

- Better rates are available as credit improves

💡 Best for: Buyers close to the 620+ range who want to avoid FHA mortgage insurance.

4. Non-QM & Alternative Loan Options

If you don’t qualify for traditional financing, there are non-QM (non-qualified mortgage) or portfolio loan options.

These may be considered:

- Bank statements instead of tax returns

- Higher debt-to-income ratios

- Unique financial situations

⚠️ Keep in mind:

- Higher interest rates

- Larger down payment requirements

- Vary widely by lender

💡 Best for: Self-employed buyers or those with more complex financial profiles.

What Lenders Look at (Beyond Credit Score)

Credit matters—but it’s not the only factor.

Lenders also evaluate:

- Income stability

- Debt-to-income ratio (DTI)

- Employment history

- Cash reserves

✨ A lower credit score can often be offset by strengths in other areas.

How to Improve Your Credit (Even in 60–90 Days)

If you’re close to qualifying, a few strategic steps can make a big difference:

- Pay all bills on time (this has the biggest impact)

- Reduce credit card balances (aim for under 30% utilization)

- Avoid opening new credit accounts

- Keep older accounts open to build credit history

- Check your credit report for errors and dispute inaccuracies

💡 Even a small increase in your score can improve your loan options and interest rate.

Should You Wait-or Buy Now?

This depends on your situation.

👉 Buy now if:

- You qualify for a loan that fits your budget

- You plan to stay in the home for a few years

- You can refinance later after improving your credit

👉 Wait if:

- Your current loan options are unaffordable

- A short-term credit improvement could significantly improve your terms

Final Thoughts

You don’t need perfect credit to buy a home-you just need the right strategy and the right loan program.

With today’s options, many buyers can purchase sooner than they expected-and improve their financial position over time.

💬 If you’re wondering what you qualify for or want to explore your options, I’m happy to connect you with trusted lenders and help you map out a plan. You might be closer than you think.

Categories

Recent Posts